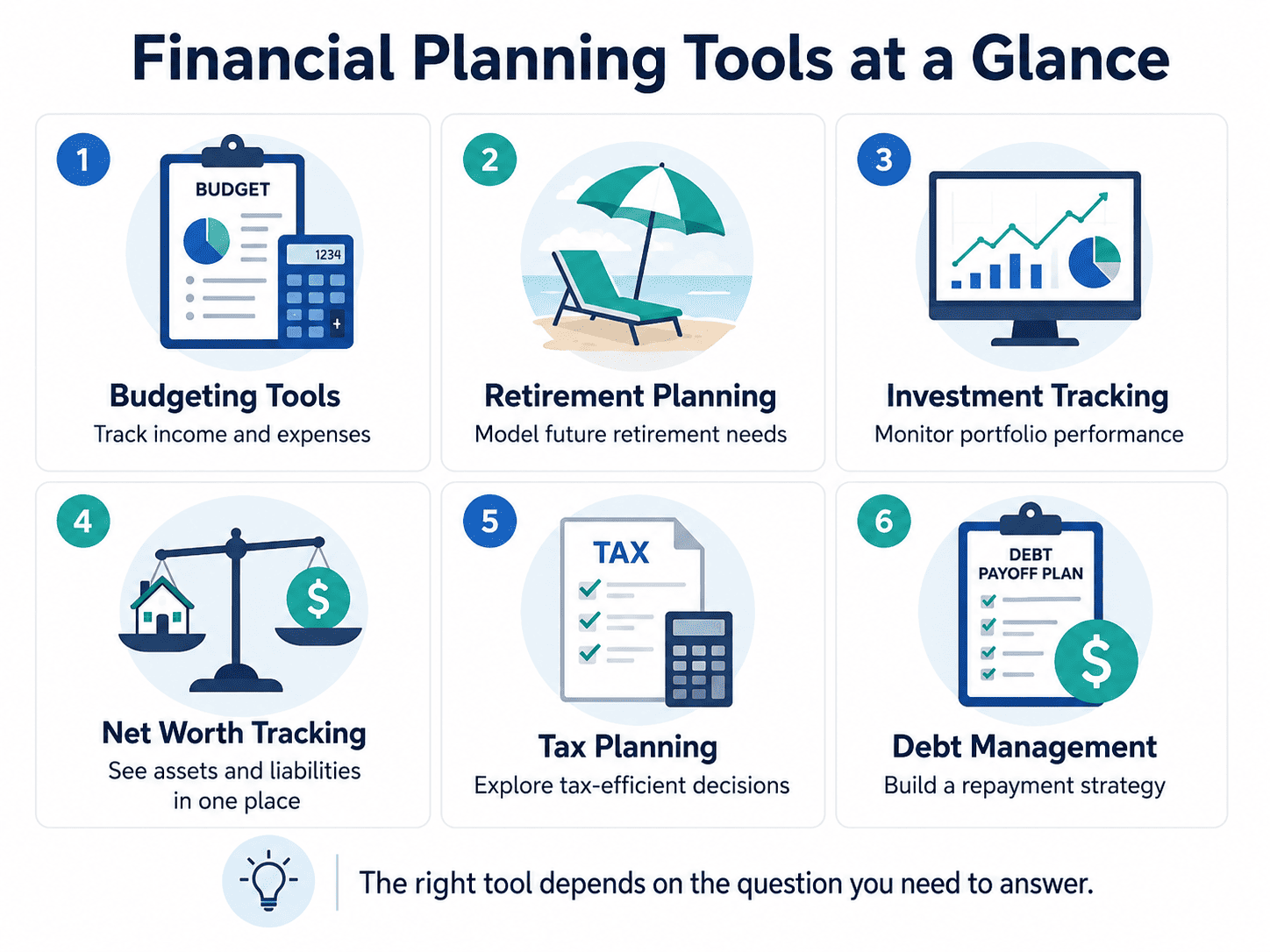

Financial Planning Tools

Managing money is not always a question of income.

You may earn enough to cover your basic needs and still struggle to save, pay off debt, or feel confident about your financial future. You may understand what you should do but find it difficult to turn that knowledge into consistent action.

Financial planning tools can make this process easier.

They help you organize financial information, understand your current situation, set goals, and make more informed decisions about spending, saving, investing, taxes, retirement, and debt.

Some tools focus on calculations. Others track accounts or show how your financial position changes over time. Newer solutions, such as AI Financial Coach, focus on financial behavior and help users choose a strategy that fits their strengths, habits, and natural way of making decisions.

In this guide, we will look at the main types of financial planning tools, how they work, and how to choose the right option for your needs.

Что представляют собой инструменты финансового планирования?

Инструменты финансового планирования — это приложения, калькуляторы, программные платформы и цифровые сервисы, которые помогают людям управлять различными аспектами своей финансовой жизни.

They may help you:

- track income and expenses;

- create a budget;

- build savings;

- plan for retirement;

- monitor investments;

- calculate your net worth;

- prepare for taxes;

- reduce debt;

- set financial goals;

- understand your financial behavior.

You may also see them described as:

- financial planning software;

- personal finance software;

- money management software;

- financial management tools;

- personal finance tools;

- money planning apps;

- budgeting and planning tools;

- financial goal planning tools.

The right tool depends on the question you need to answer.

Many people need more than one type of tool.

For example, a budgeting app can help you control monthly spending, while a retirement planner can show whether your long-term savings are on track.

An AI financial coaching tool serves a different purpose. It can help you understand why certain financial patterns keep repeating and which approach to earning, saving, or financial growth may suit you better.

How Financial Planning Tools Work

Most financial planning software is built around one or more of the following functions.

Account aggregation

Account aggregation brings information from several financial accounts into one dashboard.

Depending on the platform, you may be able to connect:

- bank accounts;

- credit cards;

- loans;

- mortgages;

- investment accounts;

- retirement accounts.

Services such as Plaid and Yodlee are often used to create connections between financial institutions and personal finance software.

This can save time because you do not have to check each account separately. It also gives you a more complete picture of your financial situation.

Some users prefer not to connect their accounts. Many financial tracking tools also allow manual data entry.

Cash flow modeling

Cash flow modeling looks at the money coming in and going out over time.

A basic budgeting app may show what happened during the current month. More advanced financial planning software can project how future income and expenses may affect your goals.

Cash flow modeling can help you explore questions such as:

- Can I afford a large purchase?

- How much can I save each month?

- What happens if my income changes?

- Can I take a career break?

- How would retiring earlier affect my finances?

- How long could my savings last?

These projections are not guarantees. They are models based on the information and assumptions entered into the tool.

Goal-based planning

Goal-based planning begins with a specific result.

Instead of simply trying to manage money better, you may choose a goal such as:

- creating an emergency fund;

- paying off a credit card;

- saving for a home;

- preparing for retirement;

- increasing your income;

- building long-term financial stability.

The tool then helps you understand what may be required to reach that goal.

Goal-based planning is useful because it connects financial decisions to something meaningful. It gives context to the numbers.

Budgeting and Expense Tracking Tools

Budgeting tools help you see how much money comes in, where it goes, and how much remains for your priorities.

They may help you:

- categorize transactions;

- set spending limits;

- plan for bills;

- identify recurring expenses;

- track savings goals;

- compare planned and actual spending.

Different budgeting apps use different methods.

Some require you to plan every dollar in advance. Others focus on automatic tracking and provide a general view of your spending.

YNAB

YNAB, which stands for You Need A Budget, uses a method called zero-based budgeting.

With zero-based budgeting, every available dollar is assigned a purpose. You may allocate money to rent, groceries, transportation, savings, debt, entertainment, or another category.

The goal is not to spend everything. The goal is to decide what each dollar needs to do before you use it.

YNAB may suit people who want to take an active role in budgeting and are willing to review their finances regularly.

It may be less suitable for someone who only wants passive expense tracking.

Monarch Money

Monarch Money combines budgeting, transaction tracking, financial goals, and net worth tracking.

It may be useful for people who want to see several parts of their financial lives in one place.

Its household features also make it relevant for couples who want to manage shared finances together.

Quicken Simplifi

Quicken Simplifi focuses on spending plans, bills, cash flow, and savings goals.

It may appeal to people who want a clear view of how much money remains after regular expenses without creating a highly detailed budget for every category.

PocketGuard

PocketGuard is designed to simplify everyday spending decisions.

It can help users estimate how much money is available after bills, savings goals, and regular expenses have been considered.

This may be useful for someone who wants a quick answer to the question:

How much can I safely spend?

Rocket Money

Rocket Money is commonly used for subscription and recurring expense management.

It can help users identify:

- forgotten subscriptions;

- repeated monthly charges;

- services they no longer use;

- increases in recurring bills.

This is useful because small regular payments can easily go unnoticed.

EveryDollar

EveryDollar also uses a zero-based budgeting approach.

It may suit people who prefer a simple monthly plan and want to allocate their income across specific spending and saving categories.

PocketSmith

PocketSmith combines budgeting with financial forecasting.

Its calendar-based approach can help users see how current financial decisions may affect future balances.

Lunch Money

Lunch Money provides budgeting, transaction tracking, and net worth monitoring.

It may be relevant for users who manage accounts in multiple currencies or prefer a flexible mix of automatic and manual tracking.

Tiller Money

Tiller Money sends financial data to Google Sheets or Microsoft Excel.

It is designed for people who prefer spreadsheets and want more control over their calculations, categories, reports, and financial dashboards.

Retirement Planning Tools

Retirement planning tools help answer an important question:

Will I have enough money when I stop working?

These tools may estimate:

- how much your savings could grow;

- how much income you may need;

- how inflation could affect your spending;

- how long your money may last;

- whether your savings rate is realistic;

- how different retirement dates could change the result.

Empower

Empower, formerly known as Personal Capital, combines account aggregation, investment tracking, net worth monitoring, and retirement planning.

It can be useful for people who have several investment and retirement accounts and want to see them in one dashboard.

Empower may also help users review their asset allocation and long-term retirement position.

ProjectionLab

ProjectionLab is designed for detailed long-term financial modeling.

It allows users to explore different scenarios, such as:

- retiring earlier or later;

- changing a savings rate;

- buying a home;

- taking time away from work;

- changing future spending;

- moving to another location;

- planning Roth conversions.

It can also use Monte Carlo simulation to test how a plan may perform under different market conditions.

What Is a Monte Carlo Simulation?

A Monte Carlo simulation tests a financial plan against many possible future outcomes.

It does not assume that investments will grow at exactly the same rate every year. Instead, it models periods of stronger and weaker market performance.

The result is usually expressed as a probability of success rather than a guaranteed forecast.

If a retirement plan has a low probability of success, the user may need to consider changes such as:

- saving more;

- retiring later;

- spending less;

- changing the investment approach;

- adjusting another assumption.

Boldin

Boldin focuses on detailed retirement planning.

It can help users model retirement income, spending, healthcare costs, taxes, and different withdrawal strategies.

It may be particularly relevant for people who are approaching retirement and need to coordinate several sources of income.

MaxiFi Planner

MaxiFi Planner focuses on lifetime financial planning.

Rather than only calculating a target retirement balance, it helps users think about sustainable spending across different stages of life.

It may also be useful for more complex decisions involving taxes, Social Security, and retirement income.

Social Security Optimization

Social Security optimization tools compare different claiming ages and household situations.

The aim is to understand how the timing of a claim may affect lifetime benefits.

This can be especially important for:

- married couples;

- people with different earnings histories;

- users deciding whether to claim early;

- people considering whether to delay benefits.

Roth Conversion Analysis

Roth conversion analysis compares the potential cost of paying tax now with the possible benefit of tax-free withdrawals in the future.

A tool may help estimate whether converting part of a traditional retirement account into a Roth account could be beneficial.

The result depends on factors such as:

- current tax rates;

- expected future tax rates;

- age;

- retirement date;

- account balances;

- other sources of income.

Because these decisions can be complex, calculations should not be treated as a substitute for professional tax advice.

Investment Tracking Tools

Investment tracking tools bring information from different accounts into one place.

They can help users monitor:

- portfolio performance;

- asset allocation;

- investment fees;

- gains and losses;

- diversification;

- progress toward financial goals.

These tools are particularly useful for people who invest through more than one broker or retirement provider.

Empower

Empower provides a combined view of investment and retirement accounts.

It can help users understand how their portfolio is divided between stocks, bonds, cash, and other asset classes.

Kubera

Kubera focuses on broader wealth and net worth tracking.

Along with traditional financial accounts, users may record assets such as:

- real estate;

- private investments;

- cryptocurrency;

- vehicles;

- business interests;

- collectibles.

It may suit people whose wealth is spread across several types of assets.

Wealthfront and Betterment

Wealthfront and Betterment combine automated investment management with goal-based planning.

They can build and manage portfolios based on a user’s goals and risk preferences.

These platforms may also use tax-loss harvesting in eligible taxable accounts.

What Is Tax-Loss Harvesting?

Tax-loss harvesting involves selling an investment that has fallen in value to offset taxable capital gains.

The proceeds are usually reinvested in a similar asset so that the investor can maintain a comparable level of market exposure.

The strategy may reduce taxes in some situations, but it does not remove investment risk. Tax rules and personal circumstances also need to be considered.

Net Worth Tracking Tools

Net worth is the difference between what you own and what you owe.

The basic calculation is:

Net worth = assets − liabilities

Assets may include:

- cash;

- savings;

- investments;

- retirement accounts;

- real estate;

- business ownership;

- valuable personal property.

Liabilities may include:

- credit card balances;

- student loans;

- car loans;

- personal loans;

- mortgages;

- other debts.

Net worth tracking gives you a broader picture of financial progress than income alone.

A person may earn a high salary but have a low net worth because of debt or high spending. Another person may have a more moderate income but steadily build wealth through saving, investing, and reducing liabilities.

Tools such as Empower, Monarch Money, Kubera, Lunch Money, and Tiller Money can help users monitor their net worth over time.

The purpose is not to compare yourself with other people. It is to understand whether your own financial position is improving.

Tax Planning Software

Tax planning software helps users explore financial decisions before a tax return is filed.

This is different from tax preparation software, which mainly records what has already happened.

Tax planning may include:

- Roth conversion analysis;

- retirement withdrawal planning;

- capital gain and loss planning;

- charitable giving strategies;

- future tax bracket projections;

- estimated tax payments.

Holistiplan

Holistiplan is primarily designed for financial advisors.

It can analyze tax information and help identify possible planning opportunities related to income, capital gains, retirement accounts, and charitable giving.

FP Alpha

FP Alpha uses artificial intelligence to support professional financial planning.

It may analyze information related to taxes, insurance, estate planning, and other financial documents.

It is designed mainly for advisors working with more complex client situations.

Tax Tools for Individuals

Individual users may find tax planning features within broader platforms such as Boldin, ProjectionLab, MaxiFi Planner, Wealthfront, and Betterment.

These tools can help users explore possible scenarios. However, they do not know every detail of a person’s legal or tax situation.

For important tax decisions, software should support professional advice rather than replace it.

Debt Management Tools

Debt management tools help users understand how long repayment may take and how much interest they may pay.

They can be used for:

- credit cards;

- personal loans;

- student loans;

- car loans;

- medical debt;

- mortgages.

Two common repayment strategies are the debt snowball method and the debt avalanche method.

Debt Snowball Method

The debt snowball method prioritizes the smallest balance first.

The user makes minimum payments on all debts and directs extra money toward the smallest balance.

After that debt is paid off, the same payment is moved to the next-smallest debt.

The main advantage is psychological momentum. Paying off an entire account can make progress feel more visible and motivating.

Debt Avalanche Method

The debt avalanche method prioritizes the debt with the highest interest rate.

This approach usually reduces the total amount of interest paid.

However, the first debt may take longer to eliminate, which can make the early stages feel slower.

Which Debt Payoff Strategy Is Better?

The avalanche method is generally more efficient mathematically.

The snowball method may be easier to follow emotionally.

The better method is often the one that the person can continue using consistently.

Budgeting tools such as YNAB and PocketGuard may support debt goals. Dedicated debt payoff calculators can also compare repayment strategies and estimated timelines.

Free Financial Planning Tools vs. Paid Options

You do not need to pay for software to begin financial planning.

Free financial planning tools may include:

- budgeting templates;

- debt payoff calculators;

- net worth calculators;

- compound interest calculators;

- retirement calculators;

- mortgage calculators;

- brokerage planning tools;

- government financial education resources.

Investor.gov and many financial institutions provide free calculators that can help answer specific questions.

Free tools may be enough when you want to know:

- how much your savings could grow;

- how long debt repayment may take;

- whether you are saving enough for retirement;

- how much a loan could cost;

- what monthly payment may be affordable.

Paid financial planning software may be more useful when you need:

- automatic account updates;

- ongoing transaction tracking;

- several goals in one dashboard;

- shared household access;

- advanced scenario modeling;

- detailed tax projections;

- greater customization.

A practical approach is to start with free tools and only pay for software when you understand which additional feature you actually need.

Financial Planning Software for Advisors

Financial advisors often use more advanced software than individual consumers.

Advisor platforms may include:

- client management;

- cash flow modeling;

- retirement projections;

- tax planning;

- insurance analysis;

- estate planning;

- account integrations;

- professional reports;

- compliance features.

Common advisor platforms include RightCapital, eMoney, MoneyGuidePro, NaviPlan, Asset-Map, Holistiplan, and FP Alpha.

RightCapital

RightCapital combines goal-based planning, retirement analysis, tax features, and client-facing tools.

It is often used by independent advisors and financial planning firms.

eMoney

eMoney supports detailed financial planning and client collaboration.

It can model assets, liabilities, income sources, spending, and long-term financial goals.

MoneyGuidePro

MoneyGuidePro uses a goal-based approach to financial planning.

It can help advisors and clients discuss essential needs, lifestyle goals, and optional future plans.

NaviPlan

NaviPlan focuses on detailed cash flow analysis.

It may be useful for more complex situations involving business income, pensions, executive compensation, or estate planning.

Asset-Map

Asset-Map presents a household’s financial situation visually.

Instead of starting with a long report, it can show assets, liabilities, income sources, insurance, and other important information on a single map.

These professional tools are designed to help advisors work with many clients. Most individuals do not need this level of complexity.

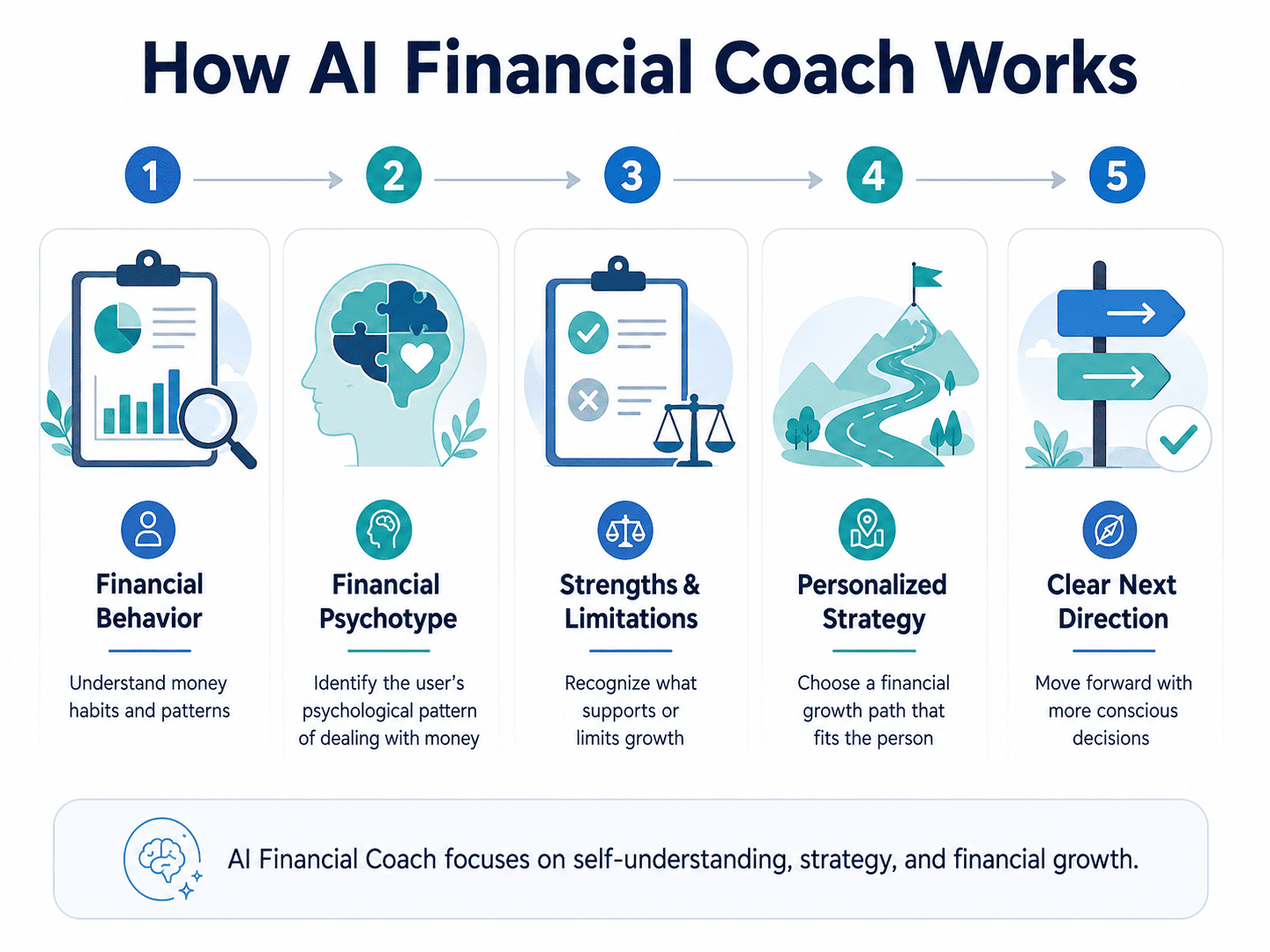

How AI Financial Coach Works

Most traditional financial planning tools focus on numbers.

They can show:

- how much you spent;

- how much you saved;

- how your investments performed;

- how long debt repayment may take;

- whether a retirement plan appears realistic.

This information is useful. But numbers do not always explain why a person keeps repeating the same financial patterns.

Two people can have similar incomes and completely different financial results.

One person may prefer stability, structure, and predictable growth. Another may earn more successfully through communication, new ideas, entrepreneurship, leadership, or rapid experimentation.

The same financial advice will not work equally well for both.

This is where AI Financial Coach is different.

AI Financial Coach Focuses on Financial Behavior

AI Financial Coach helps users understand how they think about money and which patterns influence their financial decisions.

Instead of functioning as another budget tracker, the coach focuses on questions such as:

- Why do I keep following financial strategies that do not work for me?

- What prevents me from increasing my income?

- Which strengths can support my financial growth?

- Which habits or internal patterns limit my progress?

- What kind of financial strategy fits the way I naturally think and act?

The aim is not only to tell users what happened with their money.

The aim is to help them understand why it happened.

Identifying Your Financial Psychotype

One of the central functions of AI Financial Coach is identifying the user’s financial psychotype — their psychological pattern of dealing with money.

A financial psychotype reflects recurring patterns in how a person:

- makes financial decisions;

- responds to risk;

- looks for income opportunities;

- approaches planning and stability;

- uses personal strengths;

- reacts to uncertainty;

- takes or avoids financial responsibility.

A psychotype is not a rigid label and does not define everything a person can or cannot do.

Instead, it provides a clearer way to understand why some financial strategies feel natural, while others are difficult to maintain.

Understanding your financial psychotype can also help explain why a strategy that works well for someone else may not produce the same result for you.

Recognizing Strengths and Limitations

AI Financial Coach helps users identify qualities that may support financial growth.

These may include:

- strategic thinking;

- communication;

- creativity;

- discipline;

- leadership;

- analytical ability;

- relationship building;

- the ability to notice opportunities;

- the ability to create stable systems.

The coach also helps users notice patterns that may hold them back.

For example:

- constantly changing direction;

- avoiding financial responsibility;

- choosing strategies that do not match personal strengths;

- following other people’s models of success;

- losing motivation when a process becomes repetitive;

- remaining in a familiar but financially limited role;

- expecting one universal method to solve every financial problem.

The purpose is not to judge these patterns.

It is to make them visible so that users can work with them more consciously.

Building a Personalized Financial Growth Strategy

After identifying the user’s psychotype, strengths, and recurring patterns, AI Financial Coach helps form a more personalized financial growth strategy.

The strategy may focus on areas such as:

- increasing income through existing strengths;

- choosing a more suitable professional direction;

- creating an additional source of income;

- improving the way the user makes financial decisions;

- changing patterns that repeatedly limit growth;

- choosing goals that match the user’s real priorities;

- turning general intentions into a clearer development path.

The coach does not assume that everyone needs the same solution.

For one person, growth may come from building a stable system and following it consistently.

For another, it may come from launching a new project, developing a personal brand, moving into leadership, expanding a business, or using communication skills more effectively.

Example: Choosing the Right Path to Income Growth

Imagine a person who wants to increase their income.

They have tried investing, studying different financial instruments, and following popular money strategies. They start with enthusiasm but quickly lose interest.

A standard financial tool may show their income, expenses, and investment results.

AI Financial Coach looks at a different question:

Why does this person repeatedly choose strategies they do not want to continue?

The analysis may show that their main strengths are:

- communication;

- generating ideas;

- seeing opportunities;

- building relationships;

- starting new initiatives.

Their financial psychotype may suggest that they are more likely to grow through active creation, communication, and opportunity development than through passive strategies alone.

In this case, passive investing may not be the most suitable primary path to income growth.

A more realistic strategy could involve:

- consulting;

- sales;

- entrepreneurship;

- partnerships;

- launching a service;

- developing a team;

- creating new professional opportunities.

The goal is not to recommend one specific profession to every user.

The goal is to help each person see which path is more consistent with their psychotype, natural strengths, and financial behavior.

AI Financial Coach vs. a Budgeting App

A budgeting app answers:

Where did my money go?

AI Financial Coach helps the user explore:

Which patterns influence my financial decisions, and why do I keep repeating them?

AI Financial Coach vs. a Financial Calculator

A calculator answers:

How much money could I have in the future?

AI Financial Coach helps the user explore:

Which strategy gives me the best chance of growing financially based on my psychotype, strengths, and behavior?

AI Financial Coach vs. a Financial Advisor

A financial advisor may provide professional recommendations related to:

- investments;

- retirement;

- taxes;

- insurance;

- estate planning;

- portfolio management.

AI Financial Coach has a different role.

It helps the user understand:

- financial behavior;

- internal limitations;

- personal strengths;

- financial psychotype;

- patterns affecting income;

- suitable directions for financial growth.

It is not a replacement for professional investment, legal, or tax advice.

It is a tool for self-understanding, strategy, and more conscious financial decisions.

Mint Alternatives After the Shutdown

Mint was discontinued by Intuit in October 2023.

Many former users began looking for tools that could provide budgeting, transaction categorization, account aggregation, and net worth tracking.

Possible Mint alternatives include:

- Monarch Money for household financial management;

- Quicken Simplifi for cash flow and spending plans;

- Empower for investments, net worth, and retirement tracking;

- YNAB for active zero-based budgeting;

- PocketGuard for simplified spending guidance;

- Rocket Money for subscription management;

- Lunch Money for flexible budgeting;

- PocketSmith for financial forecasting;

- Tiller Money for spreadsheet-based tracking.

The best alternative depends on how the person used Mint.

Someone who mainly tracked investments may prefer Empower. Someone who wants to change their budgeting habits may prefer YNAB. A couple managing shared finances may consider Monarch Money.

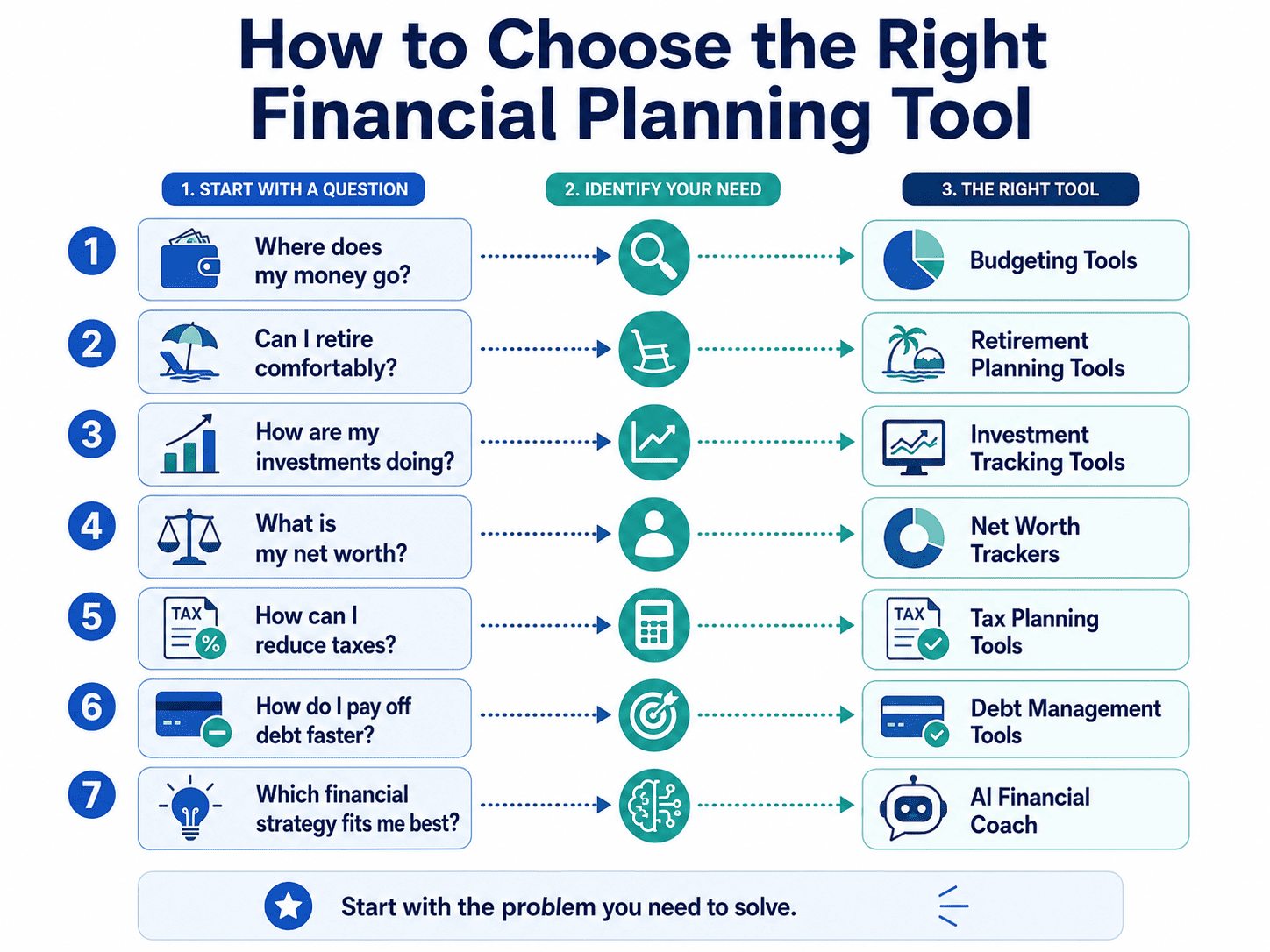

How to Choose the Right Financial Planning Tool

Do not begin by asking which platform has the largest number of features.

Begin with the problem you need to solve.

Choose Based on Your Main Question

“I do not know where my money goes.”

Start with a budgeting or expense tracking tool.

“I want to stop overspending.”

Consider a structured budgeting method such as zero-based budgeting.

“I want to see all my finances in one place.”

Look for account aggregation and net worth tracking.

“I want to know whether I can retire.”

Use retirement planning software with long-term projections and scenario modeling.

“I want to understand my investments.”

Choose an investment tracking tool that shows performance, asset allocation, and fees.

“I want to pay off debt.”

Use a debt payoff calculator and compare the snowball and avalanche methods.

“I have tried different financial strategies, but none of them feel right for me.”

AI Financial Coach may help you understand your financial psychotype, personal strengths, and the patterns influencing your financial decisions.

“I want to increase my income but do not know which direction to choose.”

A financial behavior and coaching tool may be more useful than another budgeting dashboard.

Check These Factors Before Choosing

Consider:

- your main financial goal;

- the type of problem you need to solve;

- whether you want automatic or manual tracking;

- whether you are comfortable connecting financial accounts;

- how much detail you need;

- whether you are planning alone or with a partner;

- whether a free tool is enough;

- how often you will realistically use the platform;

- whether the tool only provides information or also helps you understand what to do with it.

A complicated tool is not automatically a better tool.

The best financial planning tool is the one that helps you make clearer decisions and move toward your goals.

Final Thoughts

Financial planning is not only about choosing the right calculator or app.

A useful financial tool should help you answer at least one important question:

- Where am I now?

- Where is my money going?

- What could happen in the future?

- What is preventing me from moving forward?

- Which financial strategy is right for me?

- What should I focus on next?

Budgeting tools, retirement planners, investment trackers, tax software, and debt calculators can provide valuable financial information.

AI Financial Coach offers a different kind of support.

It helps users understand their financial behavior, identify their financial psychotype, recognize the strengths and patterns influencing their income, and choose a more personalized strategy for financial growth.

The goal is not to use as many financial planning tools as possible.

It is to choose the tools that help you understand your situation, make better decisions, and move forward in a way that works for you.

Frequently Asked Questions

- What is the best financial planning tool?

There is no single best tool for everyone. The right choice depends on your goal. Budgeting apps help manage everyday spending, retirement planners model long-term scenarios, and investment trackers monitor portfolios. AI Financial Coach is designed for people who want to understand their financial psychotype, behavior, strengths, and possible paths to financial growth.

- What are free financial planning tools?

Free financial planning tools include budgeting templates, savings calculators, debt payoff calculators, retirement calculators, net worth trackers, and compound interest calculators. They are useful for answering specific financial questions, although they may not include automatic account updates, advanced projections, or personalized guidance.

- What tools do financial planners use?

Financial planners often use professional platforms such as RightCapital, eMoney, MoneyGuidePro, NaviPlan, Asset-Map, Holistiplan, and FP Alpha. These tools may support retirement planning, cash flow modeling, tax analysis, estate planning, client reports, and account integrations.

- What happened to the Mint budgeting app?

Intuit discontinued Mint in October 2023. People who previously used Mint may consider alternatives such as Monarch Money, Quicken Simplifi, YNAB, Empower, PocketGuard, Rocket Money, Lunch Money, PocketSmith, or Tiller Money. The best replacement depends on whether you mainly need budgeting, investment tracking, forecasting, or net worth monitoring.

- Is there free software for financial planning?

Yes. Many banks, brokerage firms, government websites, and financial education platforms provide free planning tools. These may include retirement calculators, mortgage calculators, debt repayment tools, and savings projections. Free software is often sufficient for basic planning, while paid platforms usually offer more detailed analysis and ongoing tracking.

- What is the best app for tracking finances?

The best app depends on what you want to track. YNAB may suit active budgeting, Monarch Money may work well for household finances, Empower may help with investments and net worth, and Tiller Money may appeal to spreadsheet users. Choose an app that solves your main financial problem rather than the one with the most features.

- How do I create a financial plan without a financial advisor?

Start by listing your income, regular expenses, assets, and debts. Then choose one or two clear financial goals and decide what actions you can realistically take. Use a budgeting, debt, investment, or retirement tool to support your plan. Review your progress regularly and adjust the plan when your circumstances change.

- What is the difference between financial planning software for individuals and advisors?

Software for individuals usually focuses on personal budgeting, investments, debt, retirement, net worth, and financial goals. Advisor software includes more advanced features, such as client management, detailed cash flow modeling, professional reports, tax and estate planning, compliance tools, and integrations with other financial systems.

- What is the best retirement planning tool?

The best retirement planning tool depends on the level of detail you need. Empower may be suitable for a broad view of accounts and retirement progress. ProjectionLab can help with detailed scenario modeling, while Boldin and MaxiFi Planner may be more useful for retirement income, taxes, Social Security, and withdrawal decisions.

- How do financial planning tools work?

Financial planning tools organize financial information and use it to create calculations, reports, or future projections. Some connect to bank and investment accounts, while others require manual data entry. AI Financial Coach works differently: it helps users understand their financial psychotype, behavioral patterns, strengths, and suitable directions for financial growth.